Dollar down again as US job market weaker than thought

Headlines

* FOMC minutes point to “likely” rate cut coming in September

* GBP climbs to new yearly high above 1.31, EUR posts high at 1.1174

* Major downward revisions to US jobs likely pushes the Fed to act

* Gold continues to consolidate, remaining above $2500

FX: USD fell again for a fourth straight day to a low at 100.92, a level last seen in late December. The major bottom is 100.61. The Fed minutes said it would likely be appropriate to ease policy in September if data continued to come in as expected. Some saw a “plausible case” for a July 25bps cut based on progress in the jobless rate and inflation. Major downward revisions to US jobs, now averaging 178,000 instead of 246,0000 in the 12 months to March 2024, also now put pressure on the policymakers to act. Attention is next on the weekly jobless claims data later today, ahead of Powell on Friday.

EUR pushed up to a new year-to-date peak above 1.1170 as it rallied for a fourth day. The ECB’s Panetta hopes the central bank cut rates again in September. Today sees the PMIs and ECB minutes.

GBP outperformed, up for a fifth day in a row and making new highs at levels last seen in July 2023. Trend momentum signals are bullishly aligned and could keep cable on track for a shot at 1.3140.

USD/JPY was whippy and eventually closed very marginally higher on the day. Treasury yields dipped again.

AUD closed slightly lower on the day in a relatively narrow range day. The cycle high is 0.6798. USD/CAD looks to have found at its 200-day SMA, now at 1.3597.

US Stocks: US markets saw modest strength in a choppy day. The benchmark S&P 500 closed up 0.42% at 5,621. The tech-dominated Nasdaq 100 finished higher by 0.53% at 19,825. The Dow Jones settled 0.13% up at 40,890. Financials was the only sector in the red with energy pretty much flat, while consumer discretionary stocks led the gains. Target beat on profit and sales, plus it raised its guidance for EPS. The flip side was Macy’s where same store sales disappointed and it revised down its sales outlook.

Asian stock futures are mixed. Asian stocks were muted with little lead from Wall Street. The ASX 200 fell with sliding energy and oil prices hurting the sector. The Nikkei 225 initially slumped with currency strength concerning some. The Hang Seng and Shanghai Composite sunk with JD.com’s double-digit decline hitting tech. This came on news Walmart is seeking to sell off its $3.5bn stake.

Gold dipped after printing a record peak at $2531 on Tuesday. But again, prices held above the psychological level of $2500 and a long-term upward trendline.

Day ahead highlight – PMIs

PMIs provide a good lead indicator of the respective economy, specifically of the health of the manufacturing and services sectors, and of overall economic activity. The figures are calculated from a survey of purchasing managers with 50 being the critical expansion/contraction level.

The eurozone PMIs are the most widely followed, as for example in the US, the ISM data has typically been more important. The EZ composite figure fell in July, marking two months of broad-based declines and the start of a reversal in sentiment, though it remains just in expansionary territory at 50.2. Manufacturing is forecast to dip slightly to 45.6 from 45.8 and services to 51.0 from 51.9. The French Olympics effect may help the latter, but services appear to be losing steam with weak demand still keeping manufacturing in the doldrums.

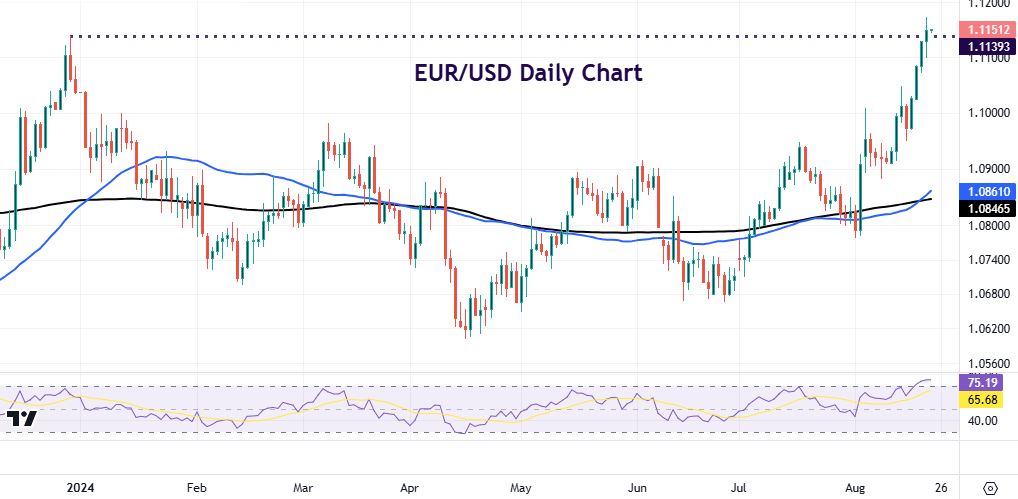

Chart of the Day – EUR/USD shoots higher

The world’s most popular currency pair has been moving north rapidly recently as the dollar side has weakened. Odds of rate cuts by both the ECB and Fed in September are nailed on, though some question if the former will go through with another move with sticky inflation a concern.

Yesterday, the major broke 1.1139, December’s peak. Very stretched intraday and daily oscillator signals suggest a pause in the EUR’s recent bull run in the near-term. Minor dips to the mid/upper 1.10s should meet some support. A continued push decisively above 1.1140 targets the low 1.12s, with the July 2023 top at 1.1276.